WASHINGTON (August 21, 2020) – Existing-home sales continued on a strong, upward trajectory in July, marking two consecutive months of significant sales gains, according to the National Association of Realtors®. Each of the four major regions attained double-digit, month-over-month increases, while the Northeast was the only region to show a year-over-year decline.

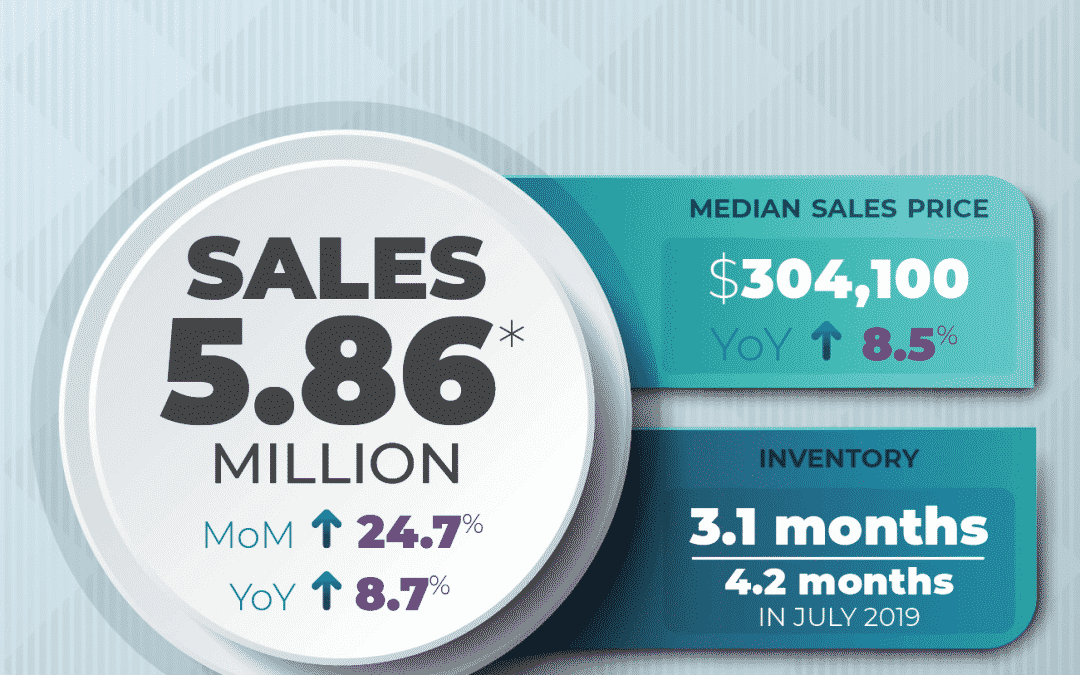

Total existing-home sales,1 https://www.nar.realtor/existing-home-sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, jumped 24.7% from June to a seasonally-adjusted annual rate of 5.86 million in July. The previous record monthly increase in sales was 20.7% in June of this year. Sales as a whole rose year-over-year, up 8.7% from a year ago (5.39 million in July 2019).

“The housing market is well past the recovery phase and is now booming with higher home sales compared to the pre-pandemic days,” said Lawrence Yun, NAR’s chief economist. “With the sizable shift in remote work, current homeowners are looking for larger homes and this will lead to a secondary level of demand even into 2021.”

The median existing-home price2 for all housing types in July was $304,100, up 8.5% from July 2019 ($280,400), as prices rose in every region. July’s national price increase marks 101 straight months of year-over-year gains. For the first time ever, national median home prices breached the $300,000 level.

Total housing inventory3 at the end of July totaled 1.50 million units, down from both 2.6% in June and 21.1% from one year ago (1.90 million). Unsold inventory sits at a 3.1-month supply at the current sales pace, down from 3.9 months in June and down from the 4.2-month figure recorded in July 2019.

Yun notes these dire inventory totals have a substantial effect on sales.

“The number of new listings is increasing, but they are quickly taken out of the market from heavy buyer competition,” he said. “More homes need to be built.”

Last week, NAR released its latest data for metro home prices, which found that in 2020’s second quarter, median single-family home prices saw a 96% increase when compared to a year earlier.

Properties typically remained on the market for 22 days in July, seasonally down from 24 days in June and from 29 days in July 2019. Sixty-eight percent of homes sold in July 2020 were on the market for less than a month.

First-time buyers were responsible for 34% of sales in July, down from 35% in June 2020 and up from 32% in July 2019. NAR’s 2019 Profile of Home Buyers and Sellers – released in late 20194 – revealed that the annual share of first-time buyers was 33%.

Individual investors or second-home buyers, who account for many cash sales, purchased 15% of homes in July, up from both 9% in June 2020 and from 11% in July 2019. All-cash sales accounted for 16% of transactions in July, equal to the percentage in June 2020 and down from 19% in July 2019.

Distressed sales5 – foreclosures and short sales – represented less than 1% of sales in July, down from 3% in June up from 2% in June 2019.

“Homebuyers’ eagerness to secure housing has helped rejuvenate our nation’s economy despite incredibly difficult circumstances,” said NAR President Vince Malta, broker at Malta & Co., Inc., in San Francisco, Calif. “Admittedly, we have a way to go toward full recovery, but I have faith in our communities, the real estate industry and in NAR’s 1.4 million members, and I know collectively we will continue to mount an impressive recovery.”

Realtor.com®’s Market Hotness Index, measuring time-on-the-market data and listing views per property, revealed that the hottest metro areas in July were Topeka, Kan.; Rochester, N.Y.; Burlington, N.C.; Columbus, Ohio; and Reading, Pa.

According to Freddie Mac, the average commitment rate(link is external) for a 30-year, conventional, fixed-rate mortgage decreased to 3.02% in July, down from 3.16% in June. The average commitment rate across all of 2019 was 3.94%.

Single-family and Condo/Co-op Sales

Single-family home sales sat at a seasonally-adjusted annual rate of 5.28 million in July, up 23.9% from 4.26 million in June, and up 9.8% from one year ago. The median existing single-family home price was $307,800 in July, up 8.5% from July 2019.

Existing condominium and co-op sales were recorded at a seasonally adjusted annual rate of 580,000 units in July, up 31.8% from June and equal to a year ago. The median existing condo price was $270,100 in July, an increase of 6.4% from a year ago.

“Luxury homes in the suburbs are attracting buyers after having lagged the broader market for the past couple of years,” Yun said. “Single-family homes are continuing to outperform condominium units, suggesting a preference shift for a larger home, including an extra room for a home office.”

Regional Breakdown

For the second consecutive month, sales for July increased in every region and median home prices grew in each of the four major regions from one year ago.

July 2020 existing-home sales in the Northeast rocketed 30.6%, recording an annual rate of 640,000, a 5.9% decrease from a year ago. The median price in the Northeast was $317,800, up 4.0% from July 2019.

Existing-home sales jumped 27.5% in the Midwest to an annual rate of 1,390,000 in July, up 10.3% from a year ago. The median price in the Midwest was $244,500, an 8.0% increase from July 2019.

Existing-home sales in the South shot up 19.4% to an annual rate of 2.59 million in July, up 12.6% from the same time one year ago. The median price in the South was $268,500, a 9.9% increase from a year ago.

Existing-home sales in the West ascended 30.5% to an annual rate of 1,240,000 in July, a 7.8% increase from a year ago. The median price in the West was $453,800, up 11.3% from July 2019.

The National Association of Realtors® is America’s largest trade association, representing more than 1.4 million members involved in all aspects of the residential and commercial real estate industries.

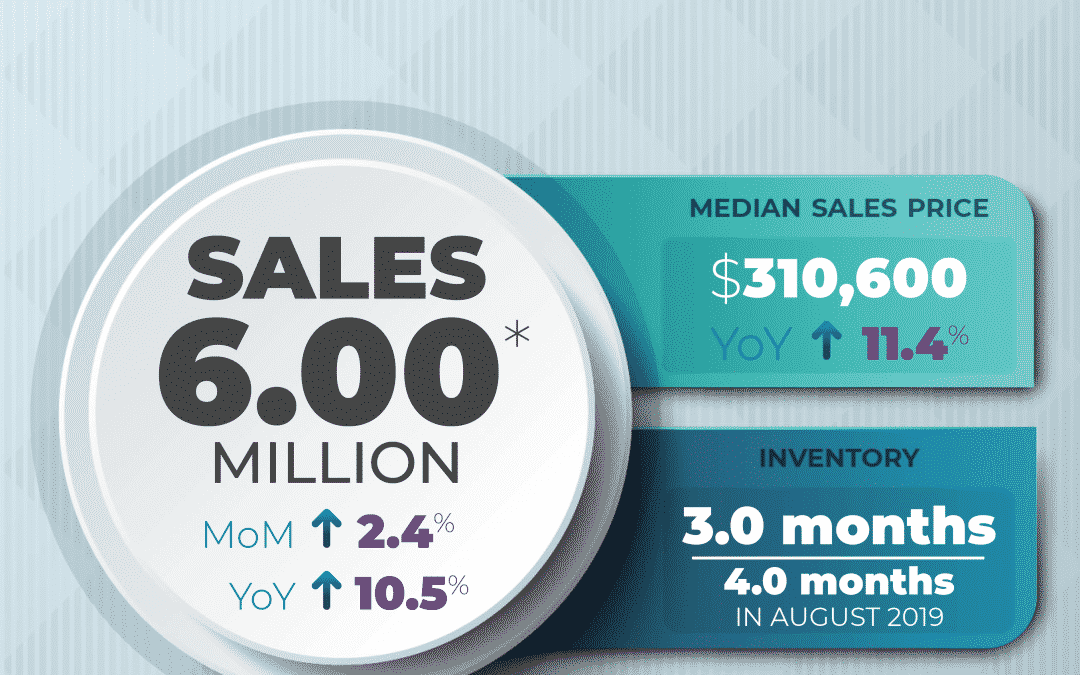

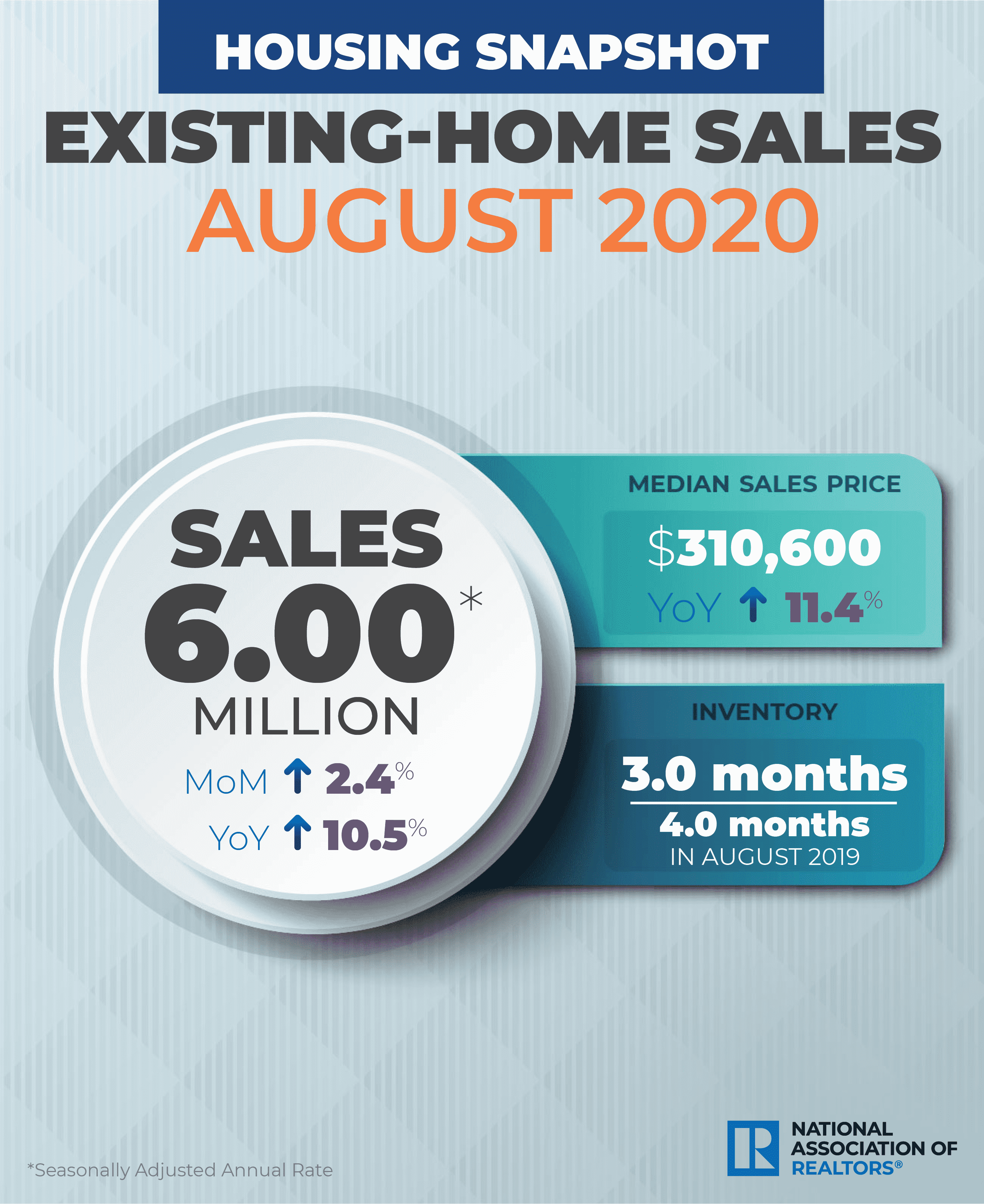

August 2020 brought 6.00 million in sales, a median sales price of $310,600, and 3.0 months of inventory. The median sales price is up 11.4% year over year, and inventory is down 1.0 month from August 2020.

August 2020 brought 6.00 million in sales, a median sales price of $310,600, and 3.0 months of inventory. The median sales price is up 11.4% year over year, and inventory is down 1.0 month from August 2020.