by Elsa Soto | Aug 28, 2018 | Blog, Buyers, Homes, Villas and Condos, Long Term Rental, News, Property for Sale in Orlando, Real Estate News, Renters

Rent Or Buy: Either Way You’re Paying A Mortgage!

There are some people who have not purchased homes because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize, however, that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

There are some people who have not purchased homes because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize, however, that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

As Entrepreneur Magazine, a premier source for small business, explained in their article, “12 Practical Steps to Getting Rich”:

“While renting on a temporary basis isn’t terrible, you should most certainly own the roof over your head if you’re serious about your finances. It won’t make you rich overnight, but by renting, you’re paying someone else’s mortgage. In effect, you’re making someone else rich.”

With home prices rising, many renters are concerned about their house-buying power. Mark Fleming, Chief Economist at First American, explained:

“Over the last three years, renter house-buying power has increased fast enough to keep pace with house price appreciation, so the share of homes that a renter can afford to buy has remained the same since 2015.

Although mortgage rates are expected to rise, they are still low by historic standards, and real household incomes are the highest they have ever been. Assuming this trend continues, our measure of affordability, which takes into account income, interest rates, and house prices, indicates that homeownership is still within reach for renters.”

As an owner, your mortgage payment is a form of ‘forced savings’ which allows you to build equity in your home that you can tap into later in life. As a renter, you guarantee the landlord is the person building that equity.

Interest rates are still at historic lows, making it one of the best times to secure a mortgage and make a move into your dream home. Freddie Mac’s latest report shows that rates across the country were at 4.51% last week.

Bottom Line

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, now may be the time to buy.

Source: Keeping Matters Current

by Elsa Soto | Aug 7, 2018 | Blog, Long Term Rental, News, Press Releases, Real Estate News

ORLANDO, Fla. – Aug. 6, 2018 – When a tenant moved out of the College Park home Ruth Zimmermann grew up in, the Los Angeles woman decided it was time to hire a Property Management Professional.

“You don’t know what you’re going to get,” Zimmermann said.

Technology is making it easier for owners to keep tabs on their properties as little or as much as they want, whether working with a management company that’s written its own app or a traditional company using common software.

Zimmermann uses Great Jones, a Fort Myers company that manages about 80 homes in Central Florida – and, like competitor Realty Medics, created its own software.

“They’re good at details and communicate with you frequently,” said Zimmermann, who also found the company to be the most plain-spoken of the ones she looked into.

Self-managing a property can work, said David Ritland of Orlando, who does that with a home he owns close to where he lives. But he turned to Realty Medics to manage a property in Deltona.

‘Farther out, when it’s going to cost me two hours round-trip to go to a site, that’s very much so worth the monthly fee to get the property managed,” said Ritland, an engineer at Siemens. Ritland said using a property manager also enables him to consider buying profitable properties that might otherwise be too distant to manage.

“The tenant has a portal they can log into, they can say, ‘Oh, something’s wrong with the microwave,’ ” Ritland said. “The next day I’m getting an email from property management and they’re saying, ‘Hey, we’ve got this idea, can we send somebody out to take a look?'”

Software such as Appfolio can be purchased by traditional property managers looking to eliminate pen-and-paper ledgers or handwritten tenant applications on clipboards.

“It takes a tenant 15 to 20 minutes to fill out an application, and it takes us less than a minute for the initial screening,” said Raul Veitia of Belmont Management Group in Winter Park and a former officer with the local chapter of National Association of Residential Property Managers.

It also enables tenants who want to pay in cash to go to a convenience store and show a code in their cellphone that can be scanned by a cashier and enable the payment to post immediately.

David Diaz, head of operations at Florida-based property management company Great Jones, talks about some useful tips for people who are thinking about being a landlord of a rental property for the first time.

“Appfolio basically can act as your accounting software, marketing software, inspections for the property have templates, and it generates reports for owners,” he said, including year-end forms such as a 1099 for taxes.

Property management is a fragmented industry because it’s localized, said Ben Sencenbaugh, president of Realty Medics, which built its own software after he joined the Orlando-based company about five years ago. It’s grown from 200 managed properties to about 900 in that time, he said.

“To get to 300 or 400 was unimaginable a couple of years ago,” said Sencenbaugh, an Embry-Riddle graduate. “We built our platform so the staff has visibility of what needs to be done – we have dashboards up on the walls in the office to show things that are overdue, things we need to attend to, high-priority items.”

Great Jones head of operations David Diaz, a UCF graduate, worked previously at Waypoint – a company that works with real estate investment trusts and manage thousands of properties. That enables such companies to keep costs low by negotiating lower expenses for repairs or buying in bulk for parts and materials or for appliances and air conditioners.

That’s part of Great Jones’ model as well as it manages about 80 properties in Central Florida and about 200 statewide.

“Property management, for whatever reason, has been a slow-to-evolve industry,” he said. “… We want to provide that same economic advantage of scale.”

Diaz, Sencenbaugh and Veitia all stressed that no software can replace personal attention for either tenants or owners. That keeps properties well managed and keeps management companies growing – as word of mouth remains the most important factor to bringing in clients.

All three companies say their business mostly involves landlords with five or fewer properties.

“It’s really about the trust factor, then having people review it and tell their friends,” Sencenbaugh said.

© 2018 The Orlando Sentinel (Orlando, Fla.), Bill Zimmerman. Distributed by Tribune Content Agency, LLC.

This is an important read when it comes to why homeowners should hire Real Estate Agents to care for their Property Management needs. At Bardell Real Estate, we offer top notch service for Property Management. Our owners and tenants have access to their online portal to effectively communicate with Property Managers, Admins and Vendors. The portal also give the tenants a great place to pay their rent, easily, and input work orders for their rental. Are you interested in receiving a Free Rental Analysis on your Orlando Vacation Home? Short term rental often offers a different spectrum from Long Term, maybe it’s time to try it out. Contact us today to obtain your FREE RENTAL ANALYSIS.

by Elsa Soto | Jul 11, 2018 | Blog, Investment Property in Florida, Long Term Rental, News, Real Estate News, Renters

ORLANDO, Fla. – July 10, 2018 – A RentCafe study that looked at average rents in many Fla. cities found that Hollywood (up 9.6 percent) and Orlando (up 8.4 percent) had the greatest year-to-year increases. Out of 19 Fla. cities included in the study, only Davie saw a year-to-year decrease (down 0.3 percent).

However, the study suggests that Davie’s average rents may be turning around. The month-to-month stat finds that they increased 0.3 percent in June. On the flipside, Coral Springs, which saw a 1.9 percent yearly increase in average rents, was the only Fla. city in the study to see rental prices decrease month-to-month in June (down 0.3 percent.)

The overall average rents for the study included studio, one-bedroom and two-bedroom apartments, which did not necessarily move the same amount. In Hollywood, for example, a one-bedroom apartment rose an average 7.1 percent year-to-year, while the average two-bedroom rose 10.9 percent.

Nationally, rents in the 250 largest U.S. cities rose 2.9 percent and reached an all-time high of $1,405. In Florida, average rents ranged from $1,018 in Lakeland to a high of $1,861 in Fort Lauderdale.

For a complete list of the 19 cities – average city rental prices by number of bedrooms plus month-to-month and year-to-year changes – visit RentCafe’s website. To view cities within the state, select “Florida” in the chart at the bottom of the page.

© 2018 Florida Realtors®

by Elsa Soto | May 16, 2018 | Homes, Villas and Condos, Investment Property in Florida, Long Term Rental, News, Property for Sale

So, how do you know if you’re ready to move from an apartment to a house? Maybe you’ve passed your step tracker hauling groceries up flights of stairs, or you simply just want the extra space for your belongings. Ask yourself these questions below to get a sense of where you’re at—or what you have to do to transition easily into home-buying mode once the time is right.

For starters, let’s talk money. Buying a home is a hefty purchase, probably the largest you’ll ever make. So, you’ll need a down payment (typically recommended to be 20% of the home’s purchase price) and steady income (i.e., a job) to pay your mortgage.

There are other costs also associated with homeownership:

- Closing costs (typically 2% to 5% of the home’s purchase price)

- Home insurance (cost varies by state)

- Maintenance

- Utilities

- Budget for unseen repairs and emergencies

While renting might seem more economical than owning at first glance, that’s not always the case; our rent vs. buy calculator can help you compare the costs. You might be surprised by the results!

Another good first step to figuring out whether you can afford a house is to enter your salary and town of residence into a home affordability calculator, which will show you how much you’d pay for a mortgage on a typical house in that area. Or talk with a loan officer or your local realtor about whether you would qualify for a mortgage, and how much you can spend comfortably. Such consultations are free, and will give you a concrete dollars-and-cents sense of where you stand.

Are you settled in your job?

Your job situation is not only important in terms of income to buy a home, but also whether you’re happy where you work and plan to stay put. Because once you own a home, your career prospects do narrow somewhat, purely because a home anchors you to one area.

“Homeowners tend to have fewer job opportunities compared to renters, since renters can easily accept a job in another city or state,” says Reid Breitman, managing partner at Kuzyk Law, in Los Angeles. “A homeowner may decline such an opportunity because they don’t want to go through the cost, time, and expense of selling their home. So, it may be better to wait to purchase a house until after you’re firmly established in your employment situation.”

Do you know where you want to live?

Since moving once you own a home is not as easy as just packing your bags (which, let’s face it, is a hassle in itself), you really need to make sure you’re picking a home in an area where you’ll be happy.

“It’s not easy to just sell a house and move to a new one if intolerable neighborhood issues come up, since the transaction cost to sell—up to 8% to 10% of the sale price for brokerage fees, escrow, title, and other costs of sale—would be relatively very expensive,” Breitman says. “So you need to really scope out the neighborhood.”

When in doubt, try renting for a few months to make sure you like the area before you start shopping for a home to own for good.

How much home maintenance are you willing to tackle?

If you love the challenge of fixing a leaky faucet and figuring out which shrubs will flourish in your yard, homeownership may be right up your alley. But if the idea of mowing a lawn or messing with the HVAC makes you depressed, then you may want to stick with renting, which gives you a roof over your head without the work.

“Apartment renters don’t have many home-related responsibilities,” explains Brian Davis, director of SparkRental, in Baltimore. “If something breaks, they call the landlord. Often, they don’t even need to worry about setting up utilities; they either come with the building, or the process is merely changing the name on an existing utility account.”

Living in a house you own is a different story. There’s no landlord to call if anything goes wrong; it’s all up to you. So you have to be either adept as a handyman, or willing to find and pay someone else to do such tasks. Or else consider buying a condo or co-op, where the lawns and public areas around your home are maintained by hired help.

Bottom line: Owning a home is a big commitment. So before you jump into it, you should have confidence that it works for your circumstances.

“No one should feel like they have to follow a template, that by reaching a certain age or having a certain number of children they need a house in the suburbs,” Davis says. “So forget the clichés and movies, and decide based on you.”

Contact one of our experienced agents at Bardell Real Estate and we are sure to walk you through the buying process. Even if this is your first-time purchase, our agents will make sure you have the knowledge you need to make an educated decision about your investment!

Source: Realtor.com

by Elsa Soto | Feb 28, 2018 | Homes, Villas and Condos, Investment Property in Florida, Long Term Rental

Real estate investing in general, and single-family real estate investing in particular, is very different from buying stocks, commodities or most other investments. Real estate is a leveraged investment that has the potential for delivering excellent returns because the cash down payment is a fraction of the retail value, yet it is also a hands-on venture where you make more decisions that affect your returns.

Key Considerations As You Plan Your Purchase

When considering your first (or next) single-family real estate investment, keep these seven pointers in mind:

1. Don’t let emotion cloud your decision making.

If most or all of your real estate experience to date has been buying and selling your personal residences, keep in mind that you were purchasing for a different purpose with a different set of criteria in those instances. Buying a home for yourself and your family is an inherently emotional endeavor. You “love” the large kitchen, your spouse is “wild about” the main floor master bedroom, the kids are “so excited” about the pool.

With investment real estate, it’s all about the numbers. If the combination of the purchase price, estimated renovation costs, expected rental income and market conditions support a purchase decision, you can feel comfortable moving forward.

2. Buy based on current returns, not future appreciation.

Will the property have a positive cash flow the day the renters move in? That’s the evaluation criteria you must use. Trusting that area rents and home values will increase over time and that that is where you’ll get your return is a recipe for disappointment, if not disaster. Optimism is an excellent personality trait, but in single-family real estate investment, it can lead to big losses. The best deals make money from day one, and long-term appreciation is a bonus.

3. Budget realistically.

As a property owner and landlord, there are expenses you will incur in order to maintain the value of your asset, so you must plan accordingly. The most obvious of these expenses is the upkeep on the property. However, there are other costs you should budget for. One that is often overlooked is vacancy expense.

In a perfect world, your property would be rented continuously with no gaps. However, the reality is that you may lose a tenant on short notice and have to pay the mortgage for a month or two before a new tenant has moved in. If you have not budgeted for vacancy expense, this interruption in your cash flow can come as an unwelcome surprise and a hit to your financial planning.

4. Know your sub-markets/neighborhoods.

Choosing to make a single-family rental investment in a particular metropolitan area simply because a national article states the market, in general, is positive can backfire if you don’t get the details on the specific sub-market or neighborhood where you intend to buy. While the key financial indicators for a city such as job growth, population growth and others may be on the rise overall, that doesn’t guarantee that the specific community you are interested in is enjoying the same kind of upswing. In fact, one sub-market may be growing because businesses are moving there from the area you have in mind. Be sure you have an in-depth understanding of all the forces at work. The key to success in real estate has always been location, location, location.

5. Learn about local regulations and federal laws.

All forms of investing are governed by regulations. However, with stocks and commodities, understanding those regulations is your broker’s job. In real estate investing, the responsibility for understanding everything from local annual registration and inspection requirements to federal fair housing laws falls to you. The time to learn about these legal issues is before you make your purchase. Failing to understand your obligations until after you’ve missed a deadline or violated an ordinance can be very costly.

6. Build a relationship with a local handyman or contractor.

Every rental property will need repairs and maintenance — if not immediately, then certainly over time. Before you complete your purchase, you should invest some effort in researching and connecting with experts in the area that you can call on as needed. Waiting until a pipe bursts to find a plumber can increase both your stress level and your repair costs.

7. Set aside funds for capital expenses.

As a property owner, you will have a variety of smaller, ongoing operating expenses, everything from fixing dripping faucets to making minor repairs. But items such as rooves, HVAC units and driveways eventually wear out. These things have longer lives and higher price tags and are known as capital expenditures or “capex.” These kinds of expenses can run from thousands to tens of thousands of dollars, so it is important to budget and set money aside on a regular basis to cover them.

Preparation: The Key To Investing With Confidence

Investing in single-family rental properties can be intimidating, especially if you are new to the process. The key to forging ahead confidently as you identify, vet, purchase, update and operate a rental is having done all your homework in advance. The considerations above are a great start.

Ready to start looking at your next real estate investment? Contact your local Bardell agent to look at potential investment purchase options.

by Elsa Soto | Feb 23, 2018 | Long Term Rental, News, Property for Sale in Orlando, Renters

Is Homeownership a Part of Your American Dream?

Are You Ready for Homeownership?

According to the latest Aspiring Home Buyers Profile by the National Association of Realtors (NAR), 82% of surveyed renters desire to own a home in the future, with 80% believing homeownership is a big part of achieving their American Dream.

The profile went on to state that 50% of millennials believe that their rent will increase, with 20% believing that an increase in rent will be the catalyst that pushes them to consider buying a home vs. renewing their lease.

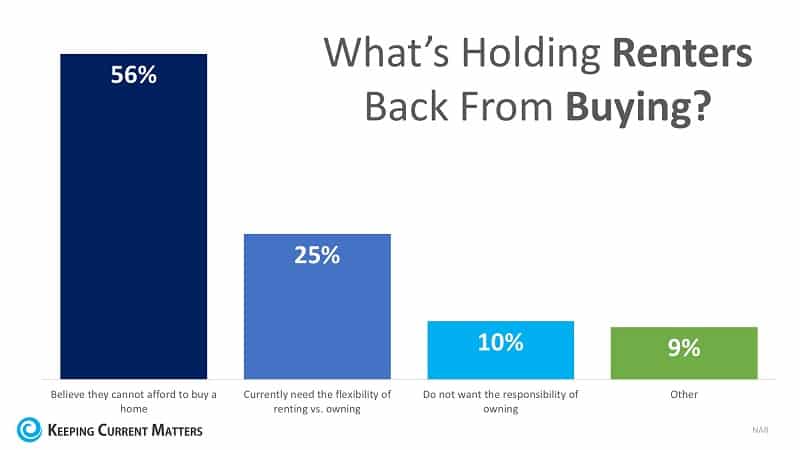

So, what is holding renters back?

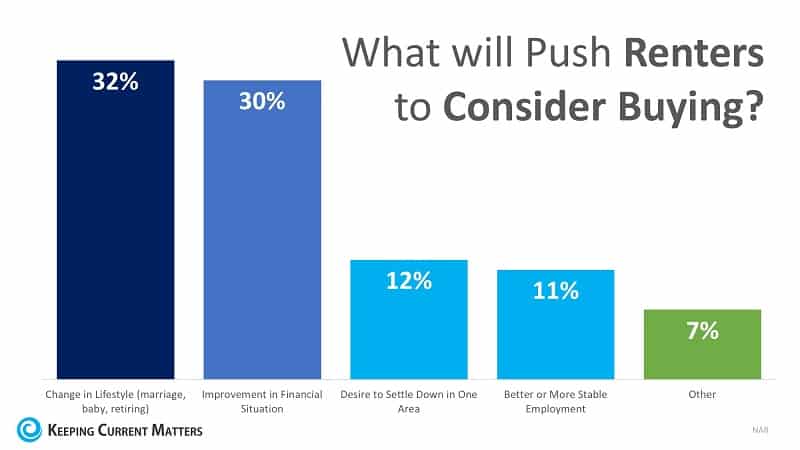

What would make renters take the plunge?

NAR’s Chief Economist, Lawrence Yun believes that,

“Housing demand in 2018 will be fueled by more millennials finally deciding to marry and have kids and the expectations that solid job growth and the strengthening economy will push incomes higher.”

Yun goes on to warn that,

“However, with prices and mortgage rates also expected to increase, affordability pressures will persist. That is why it is critical for much of the country to start seeing a significant hike in new and existing housing supply. Otherwise, many would-be first-time buyers will be forced to continue renting and not reach their dream of being a homeowner.”

So What’s The Bottom Line?

If you are one of the many homeowners whose houses no longer fit their needs and are looking to move up to your dream home, now is a great time to list your starter home! First-time buyers are out in force looking to achieve their American Dream.

Are you a currently a tenant looking to achieve your goal in 2018? Don’t wait! As home prices are on the rise along with the changing mortgage rates, now is the time to get the ball rolling. Contact your Local Bardell Realtor® today to get some more information about your home purchase!

Property Management Uses Tech to Help Landlords, Tenants

Property Management Uses Tech to Help Landlords, Tenants